Article

DOI:

https://doi.org/10.18845/te.v20i1.8408

IFRS Adoption in Colombian SMEs: An ethnographic study from an accounting management perspective

Adopción de NIIFS en Pymes comerciales en Colombia: un estudio etnográfico desde la perspectiva de gestión contable

TEC Empresarial, Vol. 20, n°. 1, (Jan - April, 2026), 82 - 107, ISSN: 1659-3359

AUTHORS

Margarita María Contreras-Cuentas

Universidad del Norte, Colombia.

mmcontreras@uninrote.edu.co.

![]()

Luis Javier Sanchez-Barrios

Universidad del Norte, Colombia.

lsanchez@uninorte.edu.co.

![]()

Yolmis Nicolas Rojano-Alvarado

Universidad de La Guajira, Colombia.

yrojanoa@uniguajira.edu.co.

![]()

Corresponding Author: Margarita María Contreras-Cuentas

ABSTRACT

Abstract

Despite the relevance of International Financial Reporting Standards (IFRS) worldwide, the literature on the aspects that SMEs need to consider after adopting such standards is scant. This study addresses the need for identifying a model that helps to guide Chief Accountants, financial controllers, and managers in similar roles to managing accounting systems after IFRS adoption. We conducted a focused ethnographic study among 26 commercial SMEs in the Colombian Caribbean Region through 36 interviews with business leaders. Through an inductive-deductive approach and iterative triangulation of data and literature, we identify a Steering Model for Accounting Management in SMEs under IFRS. Our model considers contextspecific conditions such as uncertainty, technology, teamwork, processes, and controls. Furthermore, our model underscores two managerial aspects: 1) Key IFRS topics (i.e. revenue and receivables, cash and equivalents, fixed assets, and employee benefits) and 2) Leadership (i.e. family presence in the firm, as well as technological, integral, and accounting and management). Our study not only contributes to the existing literature on managerial practices dealing with the adoption of IRS in SMEs but also sheds light to practitioners on a topic that is engraved in their role functions.

Keywords: Accounting management, IFRS adoption, ethnography, SMEs.

Resumen

Pese a la relevancia de las Normas Internacionales de Información Financiera (NIIFs) a nivel mundial, la literatura relacionada con los aspectos que las PYMEs deben considerar tras adoptar dichos estándares es aún escasa. Este estudio aborda la necesidad de identificar un modelo que oriente a los Contadores Generales, Directores Financieros y roles similares en la administración de sistemas de gestión contable luego de adoptar las NIIFs. Realizamos un estudio etnográfico focalizado entre 26 PYMEs comerciales en la Región Caribe colombiana a través de 36 entrevistas con líderes en dichas organizaciones. Adoptamos un enfoque inductivo-deductivo y triangulación iterativa de datos y literatura para definir un Modelo de Direccionamiento para la gestión contable de PYMEs bajo NIIFs. Nuestro modelo considera condiciones específicas de contexto tales como la incertidumbre, la tecnología, el trabajo en equipo, los procesos y controles. Adicionalmente, nuestro modelo resalta dos aspectos gerenciales: 1) Temas clave de las NIIFs (ingresos y cartera de clientes, efectivo y equivalentes, activos fijos y beneficios de empleados y 2) Liderazgo (familiar, tecnológico, integral, contable y de gestión). Nuestro estudio contribuye a la literatura en prácticas gerenciales en cuanto a la adopción de las NIIFs en PYMES y en términos prácticos a los roles gerenciales.

Palabras clave: Gestión Contable, adopción de NIIFs, etnografía, PYMEs.

Introduction

1. Introduction

The global development of businesses has impacted both internal corporate processes and external dynamics in the broader economy. Financial statements not only reflect economic events but also ensure legal compliance. In the case of international accounting standards, they provide the foundation for market relationships. As a result, accounting plays a significant role in achieving universal development goals (Lassou & Hopper, 2021). The International Financial Reporting Standards (IFRS) can eliminate certain accounting alternatives that are more appropriate to capture the underlying economics of business activities, especially within the unique institutional context of each country (Adhikari et al., 2021; Morais, 2020). From this perspective, principle-based accounting standards require regulators to accept a diversity of outcomes generated by different professional judgements across countries with varying political, economic, and social characteristics (Morais, 2020). This diversity poses a central concern for the International Accounting Standards Board (IASB), the main body responsible for setting global standards, which aims to promote uniformity in accounting standards worldwide (Botzem et al., 2017).

Despite the importance of IFRS, the existing literature on how Accounting managerial roles can strategically manage accounting systems after adopting such standards remain scarce. Previous studies were mostly conducted at the macro level, highlighting for instance, the usefulness of adopting IFRS in terms of reducing inefficiencies and unfair competition within the private sector; and the role of IFRS in minimizing conflicts because of different regulations and hence accounting practices worldwide (Da silva Macedo et al., 2013; Donnelly, 2007; Durán Sánchez, 2013; Lemarchand, 2002; Rodríguez Cuéllar, 2003). This is the case of the European Union (EU), where adoption of IFRS significantly shifted the financial reporting environment of publicly listed companies (Clinch & Tarca, 2008) and limited management’s opportunistic discretions (Chen et al., 2010). In the Middle East Region, adoption of IFRS aimed to improve comparability, reliability, and relevance of financial information (Aljifri & Khasharmeh, 2006). Similarly, Key and Kim (2020) found that IFRS adoption in South Korea introduced substantial changes to accounting standards with effects on the overall economy and in improving trust in financial reporting. As the second-largest capital market, Japan has strong incentives to participate in the development of international accounting standards (Kaneko & Tarca, 2008). Firms in Africa must tackle inadequate government accounting and auditing practices resulting from poor governance and regulatory frameworks (Lassou & Hopper, 2021). Previous studies in the Americas have focused on the analytical review of literature and case studies regarding regulations and documents that reflect political, institutional, and cultural features of such contexts (Beck et al., 2024; Fortin et al., 2019; Gómez-Villegas & Larrinaga, 2023; Vielma & Dymski, 2022).

As of cross-country studies, focus has been given to a) the reliability of financial statements of firms located in the Middle East and Africa (Aljifri & Khasharmeh, 2006; Lassou et al., 2021; Lassou & Hopper, 2021) and b) the impact of IFRS adoption on stock markets, particularly on the European Union (EU) and South Korea (Chen et al., 2010; Chen et al., 2023; Clinch & Tarca, 2008; Kaneko & Tarca, 2008; Key & Kim, 2020).

At a firm level, internationalization, polarized economic dynamics, and cutting-edge technologies and communications, have ushered in a new phase in accounting management in the post-adoption of IFRS. New accounting systems and selected solutions should be aligned with management systems that meet users’ needs (Ping & Sheng, 2015). This requires further understanding context-specific conditions of SMEs, which challenge traditional management practices and/or conventional markets, often characterized by functional systems and informal culture. Our ethnographic study resulted in an accounting management model after IFRS adoption in SMEs, considering their specificities. We account for human, technological, context, and key IFRS topics. Furthermore, stakeholders exert major influence on SMEs through centralized functions and processes (Gottlieb et al., 2021). These dynamics depend heavily on the legal enforcement on new accounting standards (Boz et al., 2015).

2. LITERATURE REVIEW

2.1. Adoption of IFRS in SMEs

As a result of competitive markets, firms worldwide strive to standardize the presentation of accounting policies. Financial principles, sustainability, ethical and auditing standards, and the validation of commercial accounts are key when undertaking such challenge. Therefore, international accounting standards provide an adequate arena to conduct a firm´s strategic economic analysis as well as the assessment of its strategic goals and objectives (Vetrov et al., 2017).

SMEs are essential to high, middle or low-income economies (Ayman, 2023). In 2021, the global number of SMEs was estimated at approximately 332.99 million, an increase from 328.5 million in 2019, which had previously marked the highest recorded figure for that period (Statista, 2021). However, previous studies on IFRS in SMEs remain underexplored. A total of 60 most relevant studies were published in academic journals indexed in Scopus and Web of Science between 2003 and 2024. Specifically, previous studies on IFRS adoption in SMEs reveal diverse country particularities in terms of the process per se, challenges, effects, quality, usefulness and macroeconomic considerations. Table 1 shows a selection of studies per thematic objective and research characteristics.

Table 1 Selected IFRS studies on SMEs

| Item | Thematic Objective | Description | Research Characteristics | Authors |

|---|---|---|---|---|

| 1. | Adoption and perception of IFRS for SMEs | Impact analysis of IFRS adoption regarding emergency processes and policies | - Educational process - Policy transparency - Structural analysis - Institutionality | (Wijekoon et al., 2022) |

| (Hoti & Krasniqi, 2022) | ||||

| (Sappor et al., 2023) | ||||

| (Tawiah & Gyapong, 2023) | ||||

| 2. | Specific determinants for the voluntary adoption of IFRS | Knowledge of changes in Financial Statements and new accounting techniques | - Impact of the adoption | (Atik, 2010) |

| (Uyar & Güngörmüş, 2013) | ||||

| 3. | Challenges and Harmonization of International Accounting Standards | IFRS compliance regarding new accounting knowledge and application of regulations | - Acceptance and viability of IFRS - Regulatory context | (Baldarelli et al., 2012) |

| (Svoboda, 2007) | ||||

| (Sačer et al., 2008) | ||||

| (Schutte & Buys, 2011) | ||||

| (Quagli & Paoloni, 2012) | ||||

| 4. | Effects of the Accounting Convergence Process on SMEs | Relationship between accounting and tax regulations; new governance structures | - Equity and tax impact - Governance | (Chand et al., 2015) |

| (Perera & Chand, 2015) | ||||

| (Kim & Im, 2017) | ||||

| (Sassi & Damak-Ayadi, 2023) | ||||

| (Thien & Hung, 2021) | ||||

| 5. | Quality and Usefulness of Financial Information under IFRS for SMEs | Costs and benefits of IFRS adoption and professional judgment in accounting | - Usefulness of IFRS - Biases in accounting judgements - Impact on earnings results | (Susela Devi & Helen Samujh, 2015) |

| (Susela Devi & Helen Samujh, 2015) | ||||

| (Perera & Chand, 2015) | ||||

| (Handley et al., 2018) | ||||

| (Perera et al., 2023) | ||||

| (Hsu et al., 2024) | ||||

| (Tamayo & Hernán, 2022) | ||||

| 6. | Macroeconomic and Institutional factors in IFRS Adoption | Global competitiveness of companies and complying with international accounting regulations | - Financing - Governance | (Anh & Nguyen, 2013) |

| (Bonito & Pais, 2018) | ||||

| (Zahid & Simga-Mugan, 2019) | ||||

| (Tawiah & Gyapong, 2023) | ||||

| (Muda et al., 2024) |

MSMEs (microenterprises and SMEs) in Latin America represent 90% of the business sector and generate half of all jobs. They contribute 28% of the GDP (Prensa Alegra, 2022). According to the Colombian Association of Micro, Small and Medium Enterprises (ACOPI),

MSMEs represent 99.5% of the business sector. Of these, 1.5 million are microenterprises, 103.188 are small businesses, and 27.317 are medium-sized. The commerce sector holds the largest share, with 708,094 MSMEs (Aldana Cabas, 2023). Despite this, previous studies have been mainly conducted in Australia, Turkey, Italy, New Zealand, and South Africa. Studies in the Americas have centered on audit practices; leadership styles and values; and IFRS adoption experiences (Minaburo, 2019; Mujuru, 2012).

2.2. Accounting management practices in SMEs

Management tools and accounting standards have a significant influence on policies and vice versa (Paris-dauphine, 2010). Accordingly, accounting information must reduce firm opacity and convey useful insights for decision-making (Benkraiem et al., 2022). Through simplified management, organizations can mitigate the risks of unwanted changes caused by external actors or internal personnel and understand user activities to meet compliance requirements (Haber & Hibbert, 2018). Hence accounting standards are embedded within economic and political systems that: 1) Incentivize managers to produce high-quality financial reports and 2) Enable executive monitoring through published accounts (Chen et al., 2010; Molina, 2013). Yet managers must compare the benefits with the underlying costs of IFRS adoption (Durán Sánchez, 2013). That is, the cost-benefit analysis should consider managerial challenges (e.g. learning curve, procedures, hiring experts) in relation to benefits associated with IFRS knowledge and adoption at a reasonable cost.

Accounting management is understood as decision making oriented towards financial returns in the long term; and as a key feature in business planning and control (Márquez Rondón, 2021; Parraga & Intriago, 2023). Consequently, accounting practices and accountants should be aligned with accounting management (De la Rosa, 2022). Specifically, accounting management addresses the limitations of financial information in relation to key aspects that are essential for decision-making (García Panti & Pérez Ruiz, 2015). Practices such as activity-based valuation, budgeting, or performance evaluations are useful to emphasize, improve or demonstrate organizational effectiveness (Hiebl, 2018). This results in increased profitability after implementing innovative practices that add value (Fuentes Doria et al., 2019); relying on sound budgets; and through the use of integrated information technologies such as Enterprise Resource Planning (ERP) systems that transcend a mere technological tool and are useful to present organizational strategic objectives (Abad-Segura et al., 2021; Ping & Sheng, 2015). Accounting management aims to respond dynamically and digitally to organizational challenges in real time, integrating both quantitative and qualitative information for decision-making. Company growth and an increased separation between ownership and control, shape the informative contents of financial statements as a communication tool between shareholders and managers (Brandau et al., 2017).

On the other hand, accounting management practices are performed by organizational actors who are primarily motivated by financial performance and rely on practical experience (Laguecir et al., 2020). This suggests that regulatory frameworks and national culture play key roles in accounting and finance practices. That is, what strengthens accounting and financial operations in one country may weaken them in another. This relatively unexplored area in literature motivates research on human and organizational features in relation to account management practices after the adoption of IFRS in SMEs. Particularly, its support role for business leaders in ensuring compliance with processes, policies and legislation aimed at improving business operations. Additionally, financial managers must navigate organizational challenges that include the limited use of financial statements by top management; decision-making based primarily on intuition; a lack of financial diagnosis; and minimal engagement in budgeting and financial planning (Castaño Ríos et al., 2017).

The challenges and opportunities mentioned above underscore the importance of understanding context and organizational conditions that affect accounting management practices in SMEs after the adoption of IFRS. Thus, our study focuses on the specific realities and characteristics of the SMEs under review, which are likely to be found in similar contexts. This study contributes, therefore, to understanding the unique challenges and opportunities that SME Accounting Managers face when managing accounting strategies after the adoption of IFRS. Accordingly, we identify a strategic accounting management model that will be useful for Chief Accountants, Controllers, and similar roles in SMEs.

Methods

3. Methodology

Methodologically, previous qualitative accounting studies have conducted interpretative analyses of institutional and regulatory contexts (Aburous, 2019; Ames, 2013; Chunhui Liu et al., 2011; Elbannan, 2011; Ramanna & Sletten, 2014; Silva & Nardi, 2021); bibliometric and documentary analyses (Bathla et al., 2024; Murcia & Santos, 2010; Santos & Cavalcante, 2014; Zori & Seny Kan, 2018). Other studies have been mixed (Chunhui Liu et al., 2011; de Moura & Gupta, 2019) or ethnographic (Contreras Cuentas et al., 2022; Kohler et al., 2021).

This qualitative study explores and sheds light on the managerial practices behind IFRS adoption among those that lead process and controls in SMEs. This is consistent with Älvarez and Jurgenson (2014) : “… conducting research in the real world, instead of contexts specifically created for research purposes”. Consequently, data were extracted as a result of interacting with those related to the research objective within a social context (Henry & Agafonoff, 2006), particularly, business contexts. We considered organizational culture through the interpretation of meanings, patterns, beliefs, and team membership. As suggested by (Vargas Beal, 2011), we not only allowed for openness on how to conduct it but were also vigilant in terms of following a clear process (i.e. formulation, methodological design, data collection, analysis-synthesis and conclusions). More specifically, from an anthropological perspective, “ethnography” refers not to a research method, but to the written account produced by anthropologists based on their fieldwork (Mahadevan & Moore, 2023). A “focused ethnography” occurs within a limited timeframe and has a narrow research scope. It involves a restricted subpopulation sample; targeted research questions; inclusion of internal researchers; and an emphasis on applied outcomes (Trundle & Phillips, 2023, p. 1). Hence, we describe, understand, and expose the studied phenomenon: the accounting management of commercial SMEs in the Colombian Caribbean Region in the context of IFRS adoption. See Figure 1.

According to Corral (2014) , as cited by Corral, (2017), validity and reliability criteria are embedded in each stage of the research process, across various phases (see Figure 1). These criteria draw on the frameworks developed by Contreras & Arenas (2009) , Páramo et al. (2010) , Páramo & Contreras (2014), Contreras Cuentas et al. (2022) ,and Rojano Alvarado et al. (2023) .

The study originated from the ongoing engagement with 27 participating commercial SMEs (see Appendix 1) located in the Colombian Caribbean Region. These firms represent 67% of the commercial association members within the region’s traditional wholesale channel. Such leading wholesalers within the traditional channel are members of ASABA, the Association of Grocers in Barranquilla (Páramo et al., 2010). They are indistinctively led by commercial “godfathers” who provide socioeconomic support to neighborhood shops (Contreras Cuentas et al., 2022; Cuentas et al., 2020) that have served families in the region for centuries. The studies cited before were key to deciding on the SMEs selected for this study, considering commonalities in culture and normative practices. From an ethnographic perspective, this study focused on accounting management practices that are foundational for SMEs management.

In-person visits were conducted in each organization, enabling direct field observation. The ethnographer observed participants in the field as an outsider in the business context. This standpoint was useful to preserve affective neutrality and stimulated the subjects of study to share their experiences and understand the symbolic asymmetry between the researcher and participants. Biases in terms of interpretation were tackled through a) Triangulation of participants (interviewees at different organizational levels) and b) Triangulation of methods (interviews, participant observation, documentary analysis, and informal conversations).

Additionally, a bibliographic analysis matrix comprising 1,507 data entries was developed. This matrix includes fields such as reference, topic, language, year, journal, methodology, journal ranking, summary, and document type. These source characteristics allowed triangulation and facilitated the integration of empirical findings with the relevant literature.

Interviewees included 16 accountants and 20 managers in various roles (11 owners, 2 financial managers, 7 managers, 14 accounting positions, and 2 tax auditors). See Appendix 2. Selection of interviewees was based on their leading roles in terms of policies, accounting management, and decision-making in the area under study. Assistants and other subordinates were not considered in this study given that emphasis was placed on managerial and ownership roles in the commercial SMEs under study.

Discussion guides were employed to prompt the underlying reasons behind participants’ responses, aiming for a deeper understanding of their motivations (Meyer et al., 2016). As a result, 3,404 coded statements were obtained throughout a 12-month period that included 48 sessions between 5 and 8 hours on average, each. In average, interviews per participant lasted between 45 and 120 minutes.

Some SMEs provided primary data sources: meeting minutes (useful for corroborating interview narratives), management reports, accounting policies, and general evaluation of accounting analysis. These documents enriched the field diary and the understanding of the study.

Coding was conducted systematically, following selection and analysis techniques (Restrepo, 2022), which underscore empathy and patience towards people and consider field work location (Vargas Beal, 2011). This calls for inductive-deductive methods and guides the systematic identification of data hierarchies from the particularity of data extraction. Data analysis and saturation were key to understanding the phenomenon and tackling disagreements in terms of coding. This was confirmed with two SME experts (validators), who were interviewed at the beginning and at some point of the analysis phase. The aim was to confirm facts, interpretations, and particularities of management accounting identified in the study. Two coding levels emerged, as explained below.

-

Open Coding that informed and hence are reflected in (initial and/or final) characteristics and (final) concepts. See Figure 2. Instead of isolated codes, a relational pattern emerged. The diagram clearly shows a causal path that begins with “Accounting”, a foundational discipline that leads to “IFRS adoption processes” and “IFRS convergence”. Such processes result in “IFRS concepts” and “harmonization of accounting standards”, which are part of the operational reality of “SMES and IFRS”, that tackle “differences between IFRS and previous standards”. “Decision-making” is a central node that articulates and exerts direct causal relationships towards three business management dimensions: “Accounting Management”, “Financial Management”, and “General Management”. Additional aspects related to decision-making include external “Markets” and “accounting software”, which influences “management and costs”. Other codes support SMEs process and actions. These open codes were iteratively contrasted with the thematic analysis matrix presented in the following section.

-

(Selective) Analytical and Final Coding that resulted in final characteristics and ultimately in 12 final concepts and 3 categories, as shown in Figure 3. This was achieved through saturation after using Thematic Analysis and Summary Matrices (Páramo et al., 2010).

The Thematic Analysis Matrix was useful to iteratively organize and analyze data collected from interviews and field diaries. Initial characteristics emerged in relation to research objectives. Table 2 shows an example of a result obtained from the Thematic Analysis Matrix.

Table 2: Illustrative Thematic Analysis Matrix

The Summary Matrix was key to a) Organize initial characteristics; b) Identify and c) Define emergent final characteristics that were further justified in the literature. Once saturation was achieved, final characteristics resulted in 12 final concepts embedded in three integrative categories (see Figure 3). Table 3 shows an example of a result obtained from the Summary Matrix.

Methodological reliability and confirmation were achieved through rigor and objectivity in the application of data collection and analysis methods. Three triangulation methods were used in this study: a) Data triangulation (various data sources); b) Researcher triangulation (different researchers); and c) Theory triangulation (various perspectives to interpret the dataset (Gómez, 2019; Vargas Beal, 2011). Consequently, prior to writing the results, data development was constantly monitored and contrasted with concepts. This enhanced the results obtained from observation and overall results of the study (Gomez, 2012).

Another measure taken was to generate review cues used with validators (SME experts) at an initial stage and at two different moments during the analysis. Those experts validated the saturation analysis conducted and further enhanced context details for instance, in aspects such as familial influence on managerial decisions; technology adoption and maintenance; uncertainty associated with changes; adjustment of processes; and confirmation of key accounts. Additionally, the validation process resulted in the identification of low inference descriptions, or random emerging data that were not associated with the research objectives such as informality, extended work hours and generational transitions, among others.

Results obtained from qualitative observation unveiled unique data in the context of commercial SMEs under IFRS (Zipper-Weber & Mandik, 2024). Consequently, business ethnographies contribute to understand and generate managerial tools for those leading businesses (Boden et al., 2011). Such results were presented according to saturation order and the inductive relevance of emerging characteristics and concepts.

This study was conducted in accordance with the institutional framework and guidelines established by the Ethics Committee of the Health Sciences Division at a university. The companies studied belong to an organized association, to which all interviewees are affiliated. Each participant completed and signed an informed consent for the handling and use of data.

Table 3: Illustrative Summary Matrix

| INITIAL CHARACTERISTICS | INTERVIEWEE QUOTE | FINAL CHARACTERISTIC | FINAL CHARACTERISTIC DESCRIPTION | ACADEMIC JUSTIFICATION | FINAL CONCEPT | CATEGORY |

|---|---|---|---|---|---|---|

| Decision-making, change resistance, formalization, and accounting policies | “The adoption of accounting policies was difficult because of the existing informal culture. However, it was possible to formalize policies regarding customer management, receivables, and bad debt provision. This improved accounting processes”. - Participant 1 | Decision making | The manager is conscious about applying knowledge of IFRS and the manner in which accounting policies integrate into processes, controls, and management of SMEs. | (…) performance assessment, budget formulation, definition of strategic objectives and goals (Tobón Perilla et al., 2023) | Accounting and managerial leadership | Leadership |

Results

4. RESULTS AND DISCUSSION

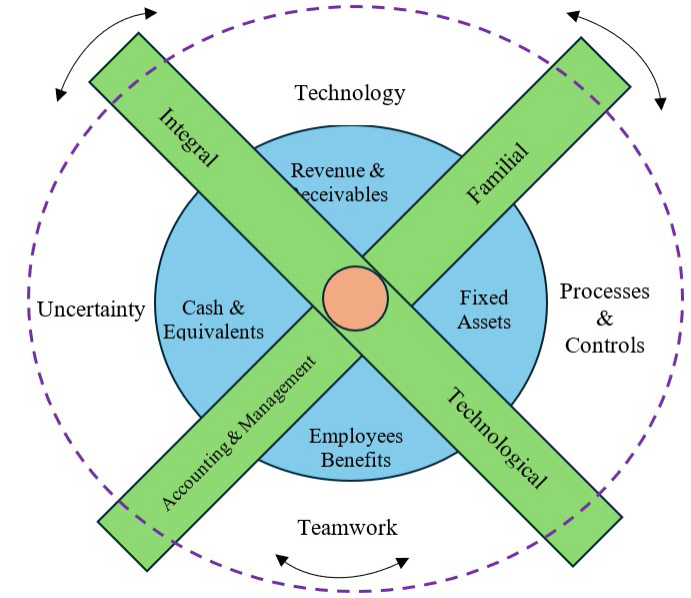

The Colombian Caribbean Region is distinctive in terms of its short-term orientation; a coastal cultural influence in management; paternalistic leadership; business informality; and a weak articulation between private and public sectors. Such distinctive features shape ethics and business decisions (Fortin et al., 2019; Kellermanns et al., 2012). Businesses that sell products and services prevail in the region, contributing in average to 40% of the regional GDP during the last 50 years (Aguilera-Díaz et al., 2013). Within the commercial sector, wholesalers and neighborhood shops provide groceries to households and other actors in the traditional channels. In average, commercial SMEs sell 47% of groceries at a low cost and conveniently (Contreras et al., 2021). These SMEs operate under an informal and fragile structure, highly shaped by informal contexts. This feature motivated our study given that despite informality, they must comply with public regulations to continue operating. Specifically, the IFRS context challenges accountants (Gómez Villegas et al., 2021; Minaburo, 2019; Vielma & Dymski, 2022) constrained by decisions made at the country central level and political networks (Beck et al., 2024). Hence understanding accounting management practices in commercial SMEs in the Colombian Caribbean Region is crucial given their unique features and context conditions: a) Internal and external aspects associated with IFRS practices; b) Key topics under IFRS; and c) Leadership. Figure 4 shows a model for Accounting Management based on the final concepts and categories explained in Section 3. It integrates internal and external factors with different types of leadership, considering key IFRS topics. The following sections explain in detail each category.

4.1. Internal and external aspects associated with IFRS practices in SMEs

IFRS adoption in the SMEs under study aligns with the provisions established in the Decree 2420 of 2015, the Sole Regulatory Decree on Accounting Standards, Financial Reporting, and Information Assurance in Colombia. This decree sets forth regulations that directly impact accounting and administrative management, incorporating various strategies to ensure organization, presentation, and use of financial statements. In such context, accountants and managers expressed:

“Eh, what can I say? I remember a lot of uncertainty, at the time I think all professionals in the field felt likewise”. -Accountant 1.

“We had some IFRS consulting… they provided us with the opening balance sheet we had to upload into the new software… we could adopt IFRS because we were organized previously to do so; otherwise, you won´t achieve it,”. -Manager 6.

Accounting reports should reflect the specificity of companies and similarly, adapt to requirements (De la Rosa, 2022) in relation, for instance, to sustainability (Contrafatto & Burns, 2013). The adoption of IFRS is more than a simple accounting exercise; it entails ramifications across multiple areas, including governance, financial management, and internal control (Thien & Hung, 2021). For a small or medium-sized enterprise, this shift represents an ongoing challenge (Aldana Cabas, 2023; Ayman, 2023). It is not merely changing the way accounting works. It requires involving all key stakeholders to ensure its implementation is aligned with the operational reality and social purpose of the organization. Moreover, commercial SMEs interact with structured suppliers and informal retailers and must adapt to different taxation requirements. A validator commented:

“… Tax regulators in other countries implemented international standards for business control purposes. In Colombia, there is a Balance Sheet for tax purposes and another for accounting purposes. What might apply according to tax regulations might not be applicable from an accounting standpoint”. -Validator 2.

The context conditions described above provide evidence that commercial SMEs do not operate under ideal IFRS accounting and administrative model. Informal practices still persist, including a commercial culture that favors verbal agreements over written contracts to support transactions. Reconciliations of tax and accounting figures and the role of family on business management impose further limitations. Therefore, commercial SMEs strive to comply with regulations under their governance conditions (Baldarelli et al., 2012; Kim & Im, 2017; Quagli & Paoloni, 2012; Sačer et al., 2008; Sassi & Damak-Ayadi, 2023). Ultimately commercial SMEs must overcome “uncertainty” related to legal and tax requirements as well as administrative processes.

Yet society adapts to organizations with slow shifts, technological advances, and emerging market trends (Abad-Segura et al., 2021). This poses further challenges in terms of data management and protection (Ru_ping & Li_sheng, 2015). SMEs and their allies -suppliers and clients with greater market share- share knowledge gained from IFRS implementation. They also integrate “technology-based” processes to obtain information that supports quantitative and qualitative decision-making. On this matter, the actors stated:

“… I experienced accounts adjustment as a usual process; I reviewed the standards and knew it had to be done. I did not feel a strong impact because it was not about money because it was still there, it was more about showing the accounting, and that was the way suppliers and banks were asking for anyway”. -Manager 4.

“…assume the accounting as mandatory… not just as an expense or an information system, but as something that will help you make better decisions”. -Manager 12.

SME leaders seek that their investments align with legal requirements. However, adapting changes needed to generate financial statements under IFRS implies higher costs. These costs are not often planned in advance due to the urgency of the operational dynamics of the business themselves. In this regard, the costs of IFRS for SMEs are associated with company size, while the benefits are not (Durán Sánchez, 2013; Litjens et al., 2012; Samuel, 2018). The validator stated:

“…each area has specific tasks, because it is unfeasible for the Accounting Department to fully monitor all areas…, the first thing is to convince managers that accounting under IFRS is everyone’s job”. -Validator 1.

Undoubtedly, accounting is a management tool, and its primary user is the company’s management, especially in SMEs and even more when they are not required to publicly present financial statements (Molina, 2013). Accounting figures turn into results, that do not merely reflect economic events, but also interdisciplinary strategic decisions which within SMEs refers to “teamwork”. Teamwork tasks include producing financial statements (Adhikari et al., 2021; H. Chen et al., 2010; Haber & Hibbert, 2018), budget allocation, and performance measurement (Hiebl, 2018).

Moreover, antagonism emerges as a result of the “one-size-fits-all” logic of IFRS for SMEs (Warren et al., 2020). That is, commercial SMEs under study strive to follow legal and IFRS models. Yet functional and informal cultures continue to permeate SME daily operations. “Processes and Controls” are required to ensure compliance with standards. A manager stated:

4.2. Key IFRS topics in SMEs

Understanding commercial sector SMEs in relation to emerging policies under IFRS prioritizes four key topics: revenue maintenance and receivables; cash and equivalents; fixed assets; and employee benefits. These areas are framed within an organizational practice system oriented toward compliance with accounting standards.

4.2.1. Revenue maintenance and receivables

One of the main challenges for commercial SMEs is client retention. According to Contreras Cuentas et al., (2022) , clients are often not only business partners but also friends and sources of personal and professional advice. Regarding IFRS use, commercial SMEs acknowledged centralized efforts to safeguard this asset, in addition to communicating the changes in requirements to clients:

“…those clients who are wholesalers continued to pay on credit. We have established certain selection criteria and credit limit assignment criteria… to filter customers and subsequently calculate portfolio impairments”. -Accountant 31.

Under IFRS, an invoice is no longer the sole relational document that supports transactions and subsequently the collection of receivables. Additional documents such as written contracts and promissory notes support the payment commitment of customers towards the company. This minimizes risk and improves collection of receivables. However, with the development of commercial invoice markets, the factoring of receivables can revitalize accumulated receivables (Chen et al., 2023). as an alternative to financing (Laguecir et al., 2020). These alternatives should result from planning and control processes (Márquez Rondón, 2021; Parraga & Intriago, 2023).

4.2.2. Cash and equivalents

Cash collection is part of the daily management strategy of commercial SMEs. It poses challenges for clients and suppliers in terms of using banks to complete transactions. This ultimately supports the broader economy. In this regard, accountants explain:

“We Pay suppliers via bank transfer. Most of the wholesale clients pay via bank transfers. In that sense, managing cash and equivalents is quite transparent”. -Accountant 18.

Cash volumes in the commercial distribution chain are high. Four policies converge to validate the use of cash: 1) Bank transfer payments to SMEs; 2) Bank transfer payments from the client to the SME’s suppliers;3) In-cash collections at the SME’s point of sale; and 4) Cash management tax regulations aligned with IFRS. These features highlight the relevance of cash management for financial and strategic purposes (Vetrov et al., 2017).

4.2.3. Fixed assets

Fixed assets in the commercial SMEs under study mainly include distribution fleet and transport equipment; repackaging machinery and equipment; and operational office equipment. In this regard, IFRS contributes to reflect realistic reasonable values instead of solely applying linear depreciation systems based on tax regulation. As an accountant explained:

“…the management of fixed assets whether such assets revaluated or appreciated. Distribution is carried with company-owned vehicles that were not previously recorded in our accounting system; currently such operating assets are included in our accounting system under IFRS”. -Accountant 23.

Therefore, asset recognition by SMEs is considered one of the achievements in presenting a more accurate reality of asset use. Consequently, this provides credible and clear information, especially for suppliers and investors (Encalada et al., 2022).

4.2.4. Employee benefits

Employees and/or leaders of commercial SMEs in the Colombian Caribbean Region manage operations that often involve long working hours. In most cases, employees are not compensated in accordance with labor laws (e.g. unpaid overtime not included in social benefits). Additionally, SMEs outsource services to loaders and freight handlers (manage goods in distribution vehicles). Bonus-based agreements are usually paid off the payroll via vouchers. This entire employee benefit structure reflects an informal context that, historically, was part SMEs operation. With the adoption of IFRS and other legal requirements, this area has now become one of attention and compliance. One accountant noted:

“…such situations are addressed from an alternative legal standpoint. You aim to preserve the concept of employees according to your current situation; look after them and pay the everything you owe the… you have to include it in employee benefits”-Accountant 8.

This corresponds to IFRS 19, which leads to more efficient decision-making (Tamayo & Hernán, 2022) (Tamayo & Hernán, 2022). Furthermore, this transcends logistical requirements and underscores that SMEs acknowledge the value of employees. This further reiterates the importance of accounting management (Benkraiem et al., 2022; García Panti & Pérez Ruiz, 2015).

4.3. Leadership

Companies implement accounting quality metrics; comparative qualitative reports; cost-benefit analyses (Barth & Lang, 2008; Bernal Muñoz et al., 2017; Chacón, 2007; Fuentes Doria et al., 2019; García Panti & Pérez Ruiz, 2015; Loaiza Robles et al., 2014). In contrast, SMEs should not rely on unplanned intuitive practices (Castaño Ríos et al., 2017). Instead, they should define strategic objectives, goals, and assess performance (Tobón Perilla et al., 2023). This facilitates the use of reports for business decision-making, operational maintenance, liquidity management and forecasting. Consequently, “accounting and management leadership” is key for IFRS adoption in commercial SMEs. In occasions it is led by the Chief Accountant, the Auditor - in some cases the Tax Auditor, and strategic team leaders.

Some accountants stated:

“80, 90% was handled by the accountant, although the final decisions were made by the administrative and general management regarding what should be adjusted, corrected, or not included”. -Accountant 17.

“Regarding the presentation [of financial statements], the current accounting software was easily adapted”. -Accountant 5.

“…for technology to go hand in hand with the process of maintaining international standards, in SMEs nowadays it is really difficult that they are not applied. Although there are still cases in which this is not the case, because they are family businesses”. -Accountant 14.

From a strategic perspective, IFRS adoption requires an “integral leadership”. Small businesses should leverage training and access to financing resources to effectively implement this model. Owners and managers should stop viewing accounting as a cost and more as an investment and an opportunity for improvement (Farfán Liévano, 2012). A manager highlighted:

“At this point, without financial statements, I don’t allow decision-making within the company”. -Manager 3.

Managerial efforts and usage of SME resources must also consider additional challenges related to governance structures. This is often a weakness due to family members representing owners in a form of “familial leadership”. Therefore, the commercial family plays a crucial role in the knowledge transfer between generations and the management team, especially when dealing with uncertainty during transitions (e.g., professionalization and succession, among others) (Giovanni et al., 2011; Hoti & Krasniqi, 2022; Sappor et al., 2023; Tawiah & Gyapong, 2023; Wijekoon et al., 2022). Managers commented:

“…this organization is complex, and this often occurs currently in commercial practice. Around ten 10 years ago we worked with consultants on designing a family protocol… We must know what is happening in the company, get involved, and make consultations on the topic”. -Manager 7.

“… generational changes involve finding harmony in what I come to say and him to trust in what had to be done…, of course, I clashed a lot, with many accountants in that moment, but my dad always trusted [me]”. -Manager 3.

Commercial SMEs in the Colombian Caribbean Region are familiar with process and managerial informality. Yet they are resilient to changing market conditions and have undertaken technological challenges. Consequently, they exhibit “technological leadership” in terms of a) adjustments based on changing regulations; and b) data systemization. IT accounting systems stimulate decision-making; convenient account transparency; and integrate with accounting knowledge (Gómez Villegas et al., 2021; Khan, 2025; Quiñónez et al., 2024). A manager stated:

“(…) At the initial stage of this business, we were the software… we then bought an accounting software for IFRS adoption… Currently, I use the software in every single way; it assists me in every single way… when the accountant considers we need to use a different software, we buy it”. -Manager 12.

Furthermore, the benefits and efficiencies of preserving financial information should outweigh costs (Dudin et al., 2015) associated with data preparation and management. This further justifies Accounting management roles. An accountant stated:

“(…) I need to remind managers and business owners that certain activities can´t be completed in that way. Permanent control and follow-up assisted by technology are key. In this industry, a common practice is like a regulation that everyone follows. Therefore, adopting policies and following procedures require effort”. -Accountant 23.

Concluding

5. CONCLUSIONS

Accounting Management is determinant for business growth; the fulfillment of corporate objectives; and the improvement of financial statements’ presentation (Barth et al., 2008; Parraga & Intriago, 2023). Consistent with existing literature on accounting management that acknowledges financial and non-financial information for decision making (Quizhpi Barbecho et al., 2019), we identify nonfinancial aspects such as leadership, teamwork, technology, managerial practices, and controlled processes among others. We further point out context conditions that affect financial information quality under IFRS, as suggested by (Chen et al., 2010).

Our study reveals that IFRS adoption entails challenges; yet adequate financial information data should lead to greater data reliability, sectorial comparability, and better strategic decision-making (Encalada et al., 2022). Decision makers in commercial SMEs who are not aware of benefits might adopt IFRS inefficiently and rather focus on implied costs (Litjens et al., 2012). This might be the result of managers adopting a partial standpoint that overlooks key aspects of IRS adoption in SMEs. We tackle this through an integrative model that sheds light on managerial aspects, that is, on how IFRS adoption occurs in SMEs, a field that is still under development.

Our accounting management practices model will benefit managers and accountants in reducing uncertainty as a result of adopting an integrated strategic vision. Specifically, our model recognizes internal and external factors that ultimately impact accounting management practices in commercial SMEs: technology, uncertainty, teamwork, processes, and controls. We identify four types of leadership: technological, familial, integral, accounting and management required for IFRS adoption. From an accounting perspective, key topics include revenue and receivables, cash and equivalents, fixed assets, and employee benefits. Resulting financial benefits include, among others: collaterals updated at fair value; updated value of receivables portfolio; and workforce formalization.

Two distinctive features of IFRS adoption in commercial SMEs were the relevance of family and the persistence of informality in certain managerial practices. The former impacts who, when, and why accounting practices occur (Gottlieb et al., 2021), as well as knowledge transfer of founding members (Giovanni et al., 2011). The latter poses a dualism for SMEs, who should incorporate organizational cultures oriented towards transparency (Quizhpi Barbecho et al., 2019).

This study provides concrete insights for practitioners. Accountants and SME managers can use the Steering Accounting Model to make direct efforts towards two key functional areas: Asset Management and Operations. More holistically, they equally benefit from the strategic nature of the model as they usually navigate internal and external factors and intertwining formal and informal conditions. Policymakers and regulatory bodies can design assistance programs to reduce the technological gap; promote the standardization of accounting processes; and ensure that graduates are qualified in at least the topics presented in this study. Regulating authorities should periodically review the standards to ensure SMEs compliance (Sappor et al., 2023). Our study stresses the importance of integrating financial and nonfinancial aspects for IFRS adoption, a relevant topic in higher and continuing education (Adhikari et al., 2021). This should promote self-reflection of accountants regarding their occupation (De la Rosa, 2022) and strategic roles in organizations.

Nevertheless, this study presents some limitations that challenge our model. First, the sample focuses on commercial SMEs in urban centers, thus excluding the realities of rural or informal sectors, where technological and cultural barriers may be more pronounced. Second, reliance on self-reported data -despite common in studies of this type- may introduce bias, in sensitive topics like normative compliance, suggesting the need to complement future studies with external audits or documented sources. Third, as a cross-sectional study, it cannot assess medium-term changes such as financial sustainability or adaptation to market fluctuations. Fourth, the implementation of our model might be hindered in SMEs with prevailing informal cultures. Yet our model might be adjusted to context-specific conditions as required.

The limitations mentioned above underscore the need for future research with diverse geographic perspectives, mixed methodologies, and broader timeframes. Further research should expand the sample to rural zones and develop a regional comparative analysis, to identify disparities based on geographical factors, such as technological access or business density. Longitudinal studies (5-10 years) should also be implemented to evaluate how sustained IFRS adoption influences competitiveness, considering variables such as investment in training or digitalization. This methodological triangulation would not only overcome temporal and geographical limitations but would support the design of differentiated policies according to regional context and organizational maturity cycles.

References